HRA is a special allowance specifically granted to an employee by his employer towards payment of rent for residence of the employee. HRA can be claimed by people who get HRA in their salaries or by individual tax payer.

How to calculate HRA :

- Actual HRA

- Rent paid(-)10% of salary for the relevant period

- 50% of salary for the relevant period (in metro cities (Delhi, Kolkata, Mumbai, Chennai)

- 40% of salary for the relevant period (other cities)

Whichever is lower is taken as HRA.

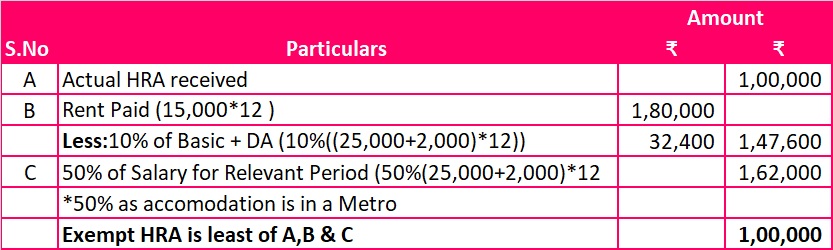

Example:

Mr. Vineesh, employed in Delhi, has taken up an accommodation on rent for which he pays a monthly rent of Rs.15,000 during the Financial Year (FY) 2019-20 i.e. Assessment Year(AY) 2020-21. He received a Basic Salary of Rs 25,000 and DA of Rs.2,000 every month. He also received a HRA of Rs.1,00,000 from his employer during the year. Let us understand the HRA component that would be exempt from income tax for the FY 2019-2020

In the above example,the entire HRA received by Mr. Vineesh (Rs.1,00,000) from his employer is exempt from income tax.

Notes:

- “Salary” for the purpose means basic salary,dearness allowance in terms of employment and commission as a fixed percentage of turnover.

- “Relevant period” means the period during which the said accommodation was occupied by the assessee during the previous year.

- Exemption is not available to an assessee who lives in his own house,or in a house for which he has not incurred the expenditure of rent. Such an assessee can claim 80GG deduction under Chapter VI-A.

71 replies on “House Rent Allowance -Section 10(13A)”

Crystal clear explaination…Keep doing the great work bro..👍👍

Good job bro….more to go ✌🏾

Well executed presentation…..Go ahead and all the very best.

Brief and concise, expecting more articles.

Great job…Do more and more and all the very best

Excellent…well explained

Well presented in simple words. Good work Irfan

Brilliant presentation….Go ahead

Well presentation…Go ahead

Brilliant work…..Do more article irfan…best of luck.

Nicely presented…..go ahead…Good luck

Well explanation…Go ahead..all the very best

Great job man….Go ahead

Nice💯

Well explained… all the best irfan

Excellent, well explained 👍

Great job 👍

Good work irfan ,go ahead , keep writing .

Nicely explained….Go ahead irfan…all the best

Executed presentation….Go ahead irfan.

Well presented article irfan….Go ahead and all the very best.

Great job….go ahead ✌

Well explained

Excellent, well explained

HRA calculation for IT is confusing to many. This article is simple with its example. Clearly explained in brief. Great job!

Now that’s what we call a presentation 🙌🙌👌👌

Way to go irfan

Well explained

Superb da….Go ahead…all the best

Great job….waiting for your next article

Nicely explained. Keep writing

Brilliant presentation…Do write more articles…Good luck.

Well explained and easy to understand

Thanks for the article irfan sv

Well executed presentation….Go ahead

Great presentation and simple expalantion….all the very best

Well explained ..go ahead irfan✌

Well explained…go ahead irfan ✌

Excellent, it’s very easy to understand ,

Well explained….expecting similar articles 💓

Well explained man…

All the best 👍

Well explained

This is great and well explained .Excellent work.

Helping one and understandable

Long way to go brother !!!! Keep writing 🙌

A clear and well understanding article explaining HRA.

Have a great future Mr.Irfan- best wishes ♥️👍🏻

Well explained Irfan.. To the point.. Long way to go man.. All the very best and looking forward for your next article

Well explained.. all the best👍

Brilliiant. U can do more and more. All the very best.

Excellent presentation with good example..all the best broo

Simple and well explained

That was really useful for my reference. Thank you

Superb… Thank you….

Well explained

I look forward to your writing 👏💯. All the best 👍

on point explanation….good work 👍

Well explained, u have narrowed down all the related points regarding HRA in a simple and elegant manner

Great👌👌👌well explained

I look forward to your writing. 💯👍

Well explained

Well explained and nearly written..Hoping to see more articles from you in future…

Good one..👍

Well explained👍

Well explained 👍

Simple and clear cut.. Go ahead man👍

Great Job.. Long way to go

Well said….go ahead irfan

Good presentation …irfan

Go ahead

All the best

Brilliant….well said…

A clear and unique presentation !! Thanks for this article Irfan Sv

Precise and to the point ! Way to go Irfan

A well executed presentation. It’s simple to understand! Love the way you present the topic. Long way to go man! All the very best!

Well explained …

All the best